If you believe the digital firewall surrounding your retirement account is a permanent shield, you are operating on obsolete assumptions.

While the mainstream financial press spends this week distracted by superficial market noise and corporate earnings theater, a massive regulatory shift quietly occurred in Washington. Over the last 48 hours straight, I have been pulling apart two heavy-duty executive orders the White House dropped on June 22, 2026.

What I found isn’t a theoretical tech problem or science fiction. It is a hard-dollar vulnerability with a fixed timeline, and it touches every single retirement account sitting behind today’s standard financial encryption.

Let me lay out the raw architecture of this threat. No simulated folksy anecdotes. No panic. Just the facts, the data rows, and the structural reality of how this systemic gap impacts your capital.

The “Harvest Now, Decrypt Later” Silent Theft

Here’s the core problem.

The encryption protecting your online brokerage, your 401(k) portal, and your digital IRA statements works perfectly fine today. But quantum computers, once they fully scale up, will crack today’s mathematical security walls like a cheap toothpick. Think of a heavy-duty combination lock, but with the master code written plainly on the back.

That’s not my cynical opinion. That is the official stance of the White House, issued on June 22, word for word:

“Ongoing cyber activity against our Nation also presents the risk of adversaries collecting United States information now, and decrypting it later once large-scale quantum computers are operational.”

Read that again. Foreign adversaries and bad actors are already actively copying your encrypted data today. Bank records, government files, and login credentials are being quietly intercepted and stored in massive digital warehouses overseas. They are simply waiting for the quantum hardware to catch up.

The intelligence world calls this strategy “Harvest Now, Decrypt Later.” I call it the largest silent theft of wealth in human history.

[ THE QUANTUM EXPOSURE TIMELINE ]

Adversary copies encrypted data TODAY ➔ Stores it in deep data warehouses ➔ Quantum computers mature ➔ Decrypts everything retroactively ➔ Your SSN, total balances, and transaction history: Wide Open.This isn’t a hypothetical drill. The federal government just set aside an estimated $7.1 billion between 2025 and 2035 to forcibly migrate its own defensive infrastructure to post-quantum encryption (PQC). Furthermore, the Department of Commerce recently signed Letters of Intent with nine major tech firms, unleashing $2 billion in direct incentives under the CHIPS and Science Act.

When Washington quietly deploys billions of dollars of taxpayer capital into a specific security upgrade, the threat is real. Period.

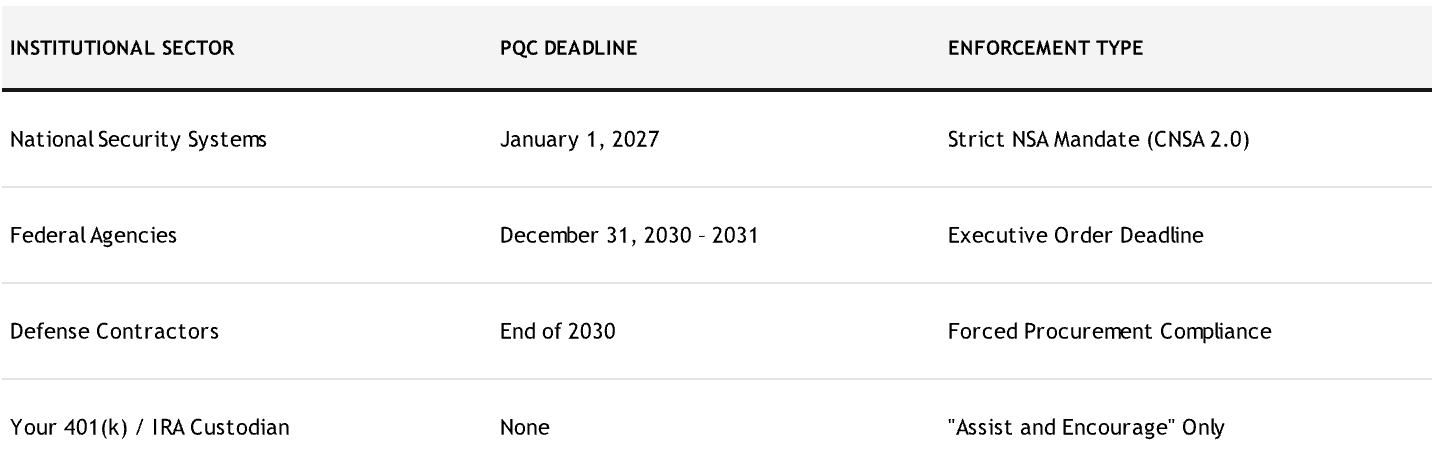

But here is the part that exposes the real systemic gap: the new executive order sets rigid, uncompromising deadlines for federal agencies, yet your private brokerage, your 401(k) custodian, and your IRA platforms have no mandatory deadline. Washington is building a multi-billion-dollar firewall around its own house, while your life savings are left standing completely out in the open.

The BS Meter — The Financial Industry's Encryption Gap

Every major financial institution will tell you they “take cybersecurity seriously.” It is printed on page 47 of every glossy annual report, usually right next to a stock photo of a lock. But turn up the BS Meter, and ask the one question they won’t answer on their own: Do they actually have a synchronized plan to deploy quantum-proof encryption?

While the private wealth sector drags its feet to protect its profit margins, look at how the national security apparatus is reacting:

The executive order merely tells agencies to “assist and encourage” critical infrastructure operators—which includes financial services. But in the real world, “assist and encourage” does not mean “secure the client’s capital by Tuesday.”

The new mandate also forces the creation of a Cryptographic Bill of Materials (CBOM) within 270 days. This will act like a nutrition label for software, listing every single encryption tool inside a product.

Right now, you have absolutely no idea what legacy encryption your brokerage is running. You can’t read the label because there is no label. The financial industry will wait until a catastrophic breach forces a regulatory mandate. Until then, your data sits behind encryption with a known, printed expiration date because no one is forcing them to upgrade.

The Arbitrage Alert — The Contract Compliance Trap

This isn’t just a data-security story; it’s a structural money story that directly impacts the value of your assets. As the federal government forces this massive PQC migration, billions of dollars will flow through highly specific channels: GSA contracts, Alliant 2, 8(a) STARS III, and the upcoming NDAA FY27 budget items.

If you hold a standard, passive target-date fund or a broad-market index fund in your retirement portfolio, you blindly own pieces of companies on both sides of this equation.

Contractor Fails PQC Compliance ➔ Loses Federal Revenue ➔ Stock Price Drops ➔ Your Index Fund Takes the Hit

The executive order explicitly states that any contractor selling to the federal government who cannot meet NIST PQC standards by the end of 2030 will lose their procurement revenue. If you hold a standard “2030 Target Date Fund,” you have no idea if you are heavy in legacy IT vendors facing a massive, unbudgeted capital expenditure to upgrade their old hardware—or if you are light in the agile cyber firms poised to capture these billions in federal deals.

The lesson here is absolute: Your brokerage statement does not show the systemic structural liabilities inside your funds. The encryption transition creates a hard line between companies that will capture government billions and companies that will be frozen out of the federal supply chain. Leaving your portfolio on passive “auto-pilot” means you are blindly absorbing the risk of legacy laggards who are running out of time.

Conclusion

The encryption protecting your life savings has a definitive shelf life. Washington just spent $7.1 billion of your money to print the expiration date, yet they left the private financial sector to police itself.

Assuming your capital is secure simply because your brokerage platform hasn’t glitched today is a terminal mistake. In a macroeconomic landscape where risk is constantly being shifted onto the retail investor, passivity is a losing strategy. You cannot fix this by trusting institutional marketing brochures or waiting for your custodian to voluntarily spend money on upgrades. You must act as your own sovereign auditor, understand the structural liabilities inside your fund allocations, and manage your perimeter with hard data.

Because when the legacy walls break down, you are entirely on your own.